By Rick Sohn, PhD

Umqua Coquille LLC

Timber Industry Report December 28, 2015

Mortgage rates remain favorable for homebuyers and warm winter temperatures favor homebuilding, for now. Log prices are high and out of balance with low product prices. Online Mortgage loans are the new kid on the block. Recent trends of lumber, home construction, and housing markets, are compared to 2006.

Interpretation and Looking Ahead.

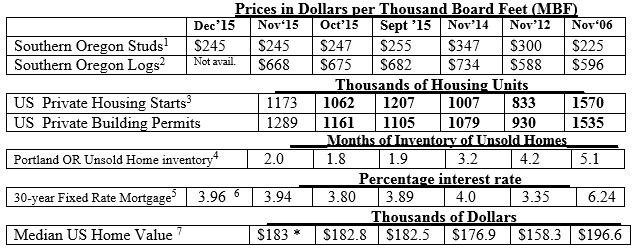

Lumber prices are stable but low. As was true last month, export from the U.S. is difficult for U.S. producers due to the high value of the dollar and the sluggishness of other economies (eg, China and Europe). Export TO the U.S. is attractive for foreign producers. This perfect storm contributes to downward pressure on prices of domestically produced wood products.

Log prices continue to drop slowly, but are still too high for the product prices. The typical upward pressure on log prices as a result of log shortages in the winter, is facing the headwinds of the weak lumber prices. It’s early in the winter, though, and sometimes the best log prices are not until in March and April, occasionally May.

Housing starts and building permits are on the upswing again, posting the second best month since 2007 (June averaged about 40,000 units higher for each). Portland unsold inventory has moved up slightly. Mortgage interest rates have held steady, despite a 0.25% interest rate hike by the Federal Reserve Board. The next 0.25% rate hike is predicted for March, with the possibility of a 1% total increase by the FED in the year 2016.

One new trend receiving attention recently is Peer-to-peer (P2P) online lending as reported by the Financial Times. Lenders are matched with borrowers through online platforms such as Lending Club, Funding Circle and Zopa, the oldest UK lending platform (which started in 2005). The loans are cheaper, quicker, and more profitable for the new lenders, who have cheaper sources of funds, such as insurers, hedge funds, and pension funds. P2P lenders are not banks, and are not required to carry regulated liquid assets, have physical branches, or deal with costly information processing systems. Currently P2P lending accounts for only 1 percent of unsecured consumer credit and small business loans, but market share is growing exponentially. The disruption of banks and other traditional mortgage lending institutions has many parallels in the disruption of traditional taxi companies by Uber and Lyft.

While most of this activity is in unsecured consumer loans, some companies are offering home mortgages, such as SoFi in the US and LandInvest and Landbay in the United Kingdom. A couple of examples: SoFi is aiming to go from $500 million in home mortgages to $3 billion next year. According to the SoFi website, SoFi is already registered to lend on property in 22 states and the District of Columbia. According to the Financial Times, Lending Club also has its sights set on home mortgages, but there is no direct information on their website.

The competition between banks and online lenders to finance mortgage loans could eventually drive mortgage interest rates down. This could increase the homebuying ability of the millennial generation and others wanting to buy.

Special Note: This month’s number for the Median U.S. Home Value is an estimate, since Zillow did not yet publish a November 30 value. According to many reports home values have slowed their increase.

Data reports used with permission of: 1Random Lengths. Recent week Kiln Dried 2×4-8′ PET #2/#2&Btr lumber. 2RISI, Log Lines. Douglas-fir #2 Sawmill Log Average, Southern Oregon region. 3 Annualized monthly. US Dept of Commerce. 4Portland, Oregon Regional Multiple Listing Service, courtesy of Janet Johnston, Prudential Real Estate Professionals, Roseburg, OR. 5Freddie Mac. National monthly average. 6 Federal Reserve Bank of St Louis Economic Research, National Average, most recent week. 7Zillow.com, National Median home value. (http://www.zillow.com/or/). Previous months and historic values are September’s figures. © Copyright Rick Sohn, Umpqua Coquille LLC. Issue #8-12. For more information, questions, or permission to reprint, please e-mail [email protected].

Disclaimer: Articles featured on Oregon Report are the creation, responsibility and opinion of the authoring individual or organization which is featured at the top of every article.